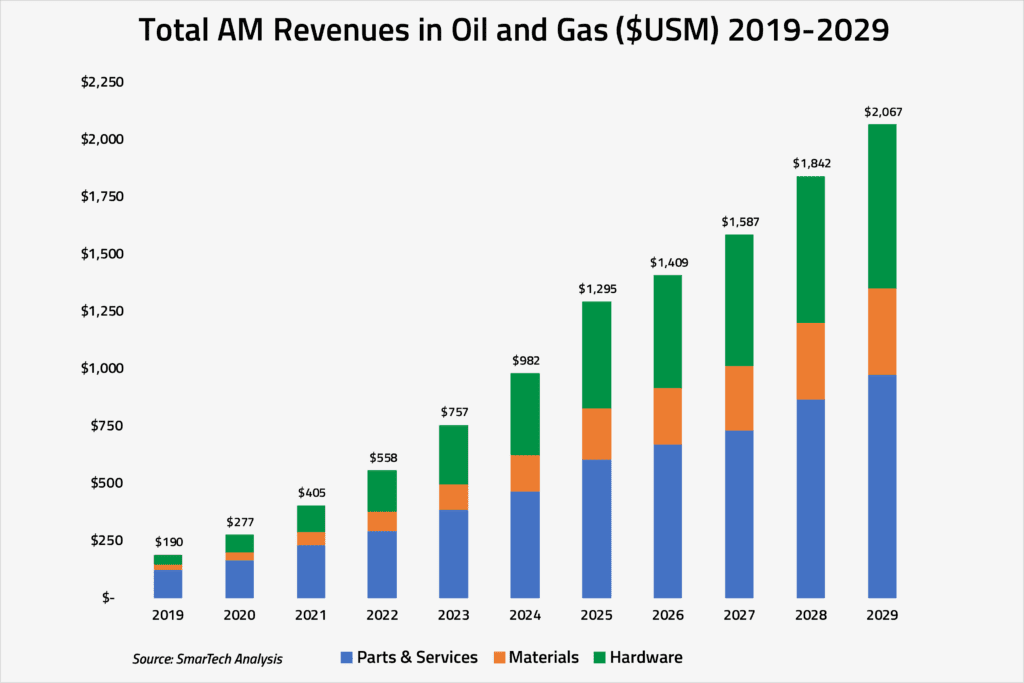

Crozet, VA: SmarTech Analysis, the leading provider of industry analysis and market forecasting data to the additive manufacturing industry, has released its latest market study of additive manufacturing in the oil and gas industry. In the report the firm reports increasing adoption of AM technologies by key oil and gas industry suppliers will result in an overall $2 billion opportunity by 2029, including a $975 million yearly revenue opportunity from AM hardware sales.

More details of the report including a table of contents and sample can be found at https://additivemanufacturingresearch.com/reports/the-market-for-additive-manufacturing-in-the-oil-and-gas-sector-2018-2029/

About the Report:

This latest edition of SmarTech Analysis’s ongoing coverage of additive manufacturing adoption in the oil and gas industry features an all-encompassing, data-driven analysis of the historic, current, and future makeup of the industry and resulting primary revenue generating opportunities.

The report assess the overall oil and gas AM opportunity, including upcoming metal, polymer, composite and ceramic AM processes and materials that are going to gain wider adoption in the oil and gas industry during the 10-year forecast period. These include leading polymer technologies for prototyping, modeling, casting and final parts, as well as high-throughput metal AM technologies such as new bound metal/binder jetting and supersonic acceleration/cold blown powder processes.

We also profile some of the leading oil and gas AM service providers, highlighting unique trends in the oil and gas market that see specialized and trusted tier 1 and tier 2 (and tier 3) suppliers (including some AM service providers) become the primary adopters of AM to provide services to the largest oil companies. Within this scenario, SmarTech Analysis expects widespread AM adoption in the oil and gas industry to be driven by hardware sales rather than by AM service providers as in other industrial segments.

For each AM segment (hardware, materials, parts and services), the ten-year, data-driven forecasts further break out the market by specific hardware technology, material type and support, part types and service provider. Over 70 fully featured data exhibits are presented in categories ranging from specific hardware technology, material type and support (metal and polymer powders, polymer and composite filaments and pellets, photopolymer resins and metal wire), part types (prototypes, tools, replacement parts and mass produced final parts) and service type (tier 1, tier 2 suppliers). Both revenue ($ Millions) and volume (units or kilograms/tonnes shipped) are considered in the forecasts.

From the Report:

• One of the key reasons why AM adoption – even after initially establishing benefits and advantages of AM – has remained relatively slow is that the largest industry stakeholders (E&P companies) entirely rely on their supply chain: tier 1 and tier 2 (even tier 3) suppliers that tend to rely on proven and effective methods of production and operation vs adopting or considering new manufacturing processes.

• The World Economic Forum has estimated that 3D printing could eventually save cost and time worth as much as $30 billion of additional value to oil and gas companies. There is significant potential value in the application of additive manufacturing and 3D printing technologies across the upstream and midstream oil and gas value chain, however it is critical that the industry identify the most valuable potential areas for use early in order to build competency and buy-in confidence to maximize potential.

• Key benefits of introducing AM hardware include tool-less manufacturing, increased geometric freedom in part design, no or less subassemblies, no physical inventory (digital warehouse), fast part availability and reduced downtimes.

• SmarTech is confirming its guidance – expressed in previous editions – that metal additive manufacturing technologies, which collectively consist on a commercial level of three major processes (as well as a number of relevant variations within these processes, with the addition of a new “cold blown powder” technology) hold the most significant potential for the oil and gas industry. Along with greater capabilities in terms of size and speed for consolidated AM technologies, significant steps forward have been made in terms of integrating additive manufacturing DED process (directed energy deposition), which can guarantee very fast production speeds through high-deposition rates and high automation in integrated hybrid (additive, measurement/inspection, subtractive) systems.

• SmarTech is confident that material development for additive manufacturing technologies is an area of potential opportunity for metal alloys and their use in industrial metal AM systems. On the other hand, development of polymer materials and support by major AM technological platforms to produce parts for the oil and gas industry is a more long-term opportunity that will require significant advancements in material science as well as a significant cost reduction of the available materials.