Formnext is over, and as usual it did not disappoint. Although the metal AM industry has been, as a whole, a bit growth challenged over the past several quarters, I believe the formnext show was effective in putting to bed any concerns about the long-term viability of additive manufacturing that may have begun to arise after some soft industry performance. The sheer scope and buy-in from large multinationals, combined with meaningful progress in the areas of automation, post processing solutions, machine productivity, and material development, continue to paint a very exciting picture for the future even as shorter-term speedbumps have continued to present challenges.

One of the most potentially interesting announcements of the show, however, came not in the form of a new machine, printable metal, innovative new software package, or exciting new application (though pretty much all of those things were being announced or demonstrated at the show). Instead, what really should have metal additive stakeholders really interested and planning around, is perhaps the first sign of real head-to-head competitiveness between two increasingly important metal additive technologies in the future.

For the last two years the bound metal printing segment has dominated the limelight with big competitive company entries, investments, and new product announcements. Despite all of this, bound metal technologies like metal binder jetting significantly lag metal powder bed fusion (and even directed energy systems) in commercial implementation. The promises and dollars behind the metal binder jetting segment, however, have at least stimulated conversations from the powder bed fusion segment concerning where metal binder jetting technologies might have a play and to what degree that might affect the existing status-quo of powder bed fusion based systems. Ultimately, these conversations helped spark SmarTech Analysis’ latest market opportunity analysis related to metal binder jetting and bound metal deposition printing technologies.

A recently announced partnership between high caliber metal AM service provider GKN Additive and “industrial burner” supplier Kueppers Solutions might be the first publicly recognizable sign that the established thinking on how metal binder jetting and powder bed fusion technologies will play together longer term is largely wrong. For most of the last few years, powder bed fusion suppliers have, for the most part, dismissed the market swell of interest in metal binder jetting technologies on the basis that these processes (as they develop) would not be directly competitive with powder bed technologies in terms of applications due to expected significant differences in the achievable mechanical properties of both approaches. After all, one is based on welding, and the other sintering -two very different metallurgical processes. There’s no getting around the fact that, indeed, both processes will produce parts with different mechanical performance profiles.

Total Projected Bound Metal Printing AM Opportunities, by Opportunity Category ($USM), 2014-2029

However, inside the announcement of the GKN/Kueppers partnership to produce burner tips was one tidbit of information that may have been mostly overlooked -the partnership will begin with a ramp up of an additively produced mixing unit in natural gas powered burner systems using laser powder bed fusion, but a next generation version of the part is eventually planned to be produced using metal binder jetting technology. Information from the two companies noted that metal binder jetting was considered an ideal match for this particular application.

It’s worth noting that powder bed fusion has made few major inroads into the industrial front, one of the most significant being gas turbine power generation and engine systems. This is one of the first -if not the first -publicly announced instances of metal binder jetting technology being planned for an application in these systems, for a part that will no doubt be exposed to a harsh operating environment, which is a role almost exclusively (until now) thought of for parts made via powder bed fusion when it comes to AM.

The implications of this, should it actually come to pass, are clear and wide reaching. Perhaps most notably, despite the metallurgical differences between the two processes method of forming parts from a metal powder, metal binder jetting will in fact be utilized for parts of a high-value and possibly critical nature -perhaps not in highly regulated industries like aerospace, but certainly in other areas which may have lower regulations as well as stricter economic constraints. Additionally, those stakeholders in powder bed fusion need to prepare for a future where their businesses may in fact become impacted by the adoption of binder jetting technology.

Most companies we’ve spoken to about this possibility over the last few years have largely dismissed the possibility. Others, such as GE Additive, may have already recognized the future implications, and are developing binder jetting solutions to complement their existing portfolio of powder bed fusion systems. Ultimately, the two technologies will likely become very complimentary, such as the scenario described by the roadmap of the GKN/Keuppers partnership. But when not in a position to benefit from this relationship, companies dedicated to one process or the other may find themselves increasingly competing for similar applications.

For the past half dozen years, additive manufacturing (AM) has presented itself to the world as an elite technology suited to grace the pages of Wired magazine, be actively discussed at Davos as part of any homage to Industrie 4.0 and helping to create impressive multi-color models displayed to great effect at trade shows of various kinds.

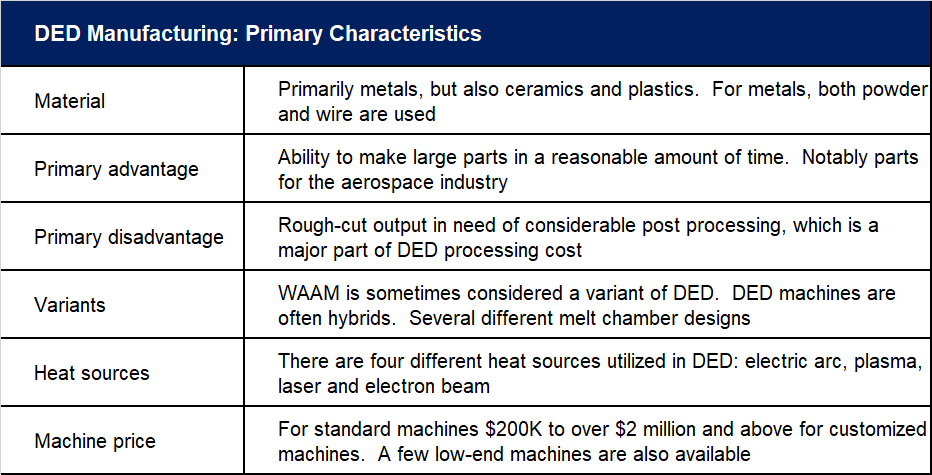

There is, however, another face of AM; more rugged and better deserving of the name “manufacturing.” It has less to do with printing and modeling and has more in common with coating and welding. There are several such processes, but most have marginal market impact or are proprietary. The exception is Directed Energy Deposition (DED).

A typical DED machine consists of a nozzle mounted on a multi-axis arm, which deposits melted material onto a surface, where it solidifies. By controlling the motion of the heat source and material feed, the melt pool is directed (hence the name of the process) through a path where it eventually freezes into solid metal. Four different heat sources are commonly utilized in DED: electric arc, plasma, laser and electron beam.

On DED Market Size

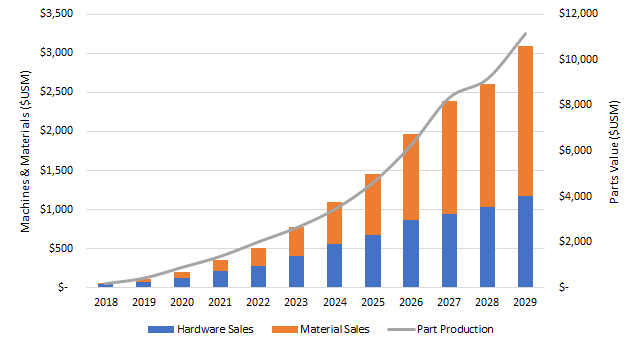

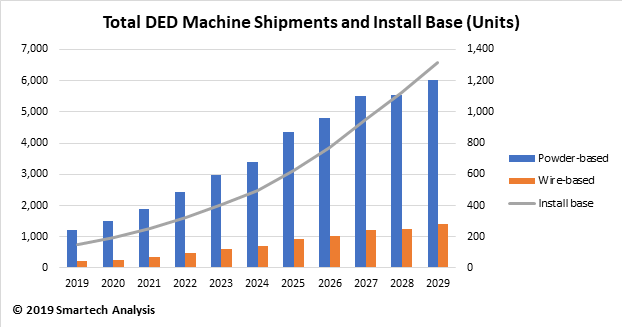

In a recent market study, Market Opportunities for Directed Energy Deposition ManufacturingSmarTech Analysis projects that the market for DED is about to take off reaching almost $490 million for the machines alone by 2025, with that year also seeing $265 million in materials being consumed by DED machines. There are about 740 DED machines installed worldwide at the present time, with that number growing dramatically to 6,590 by 2029.

These high numbers are obscured by the fact that DED is referred to by other names such as Laser Engineered Net Shaping (LENS), Direct Metal Deposition (DMD), Electron Beam Additive Manufacturing (EBAM), etc. These names vary from company to company and enable a company to distinguish itself in the market, rather than admit to being another of the herd.

Repair and Feature Enhancement as Drivers for DED

As far as which industries use – or will use – DED, it is the usual suspects – aerospace, automotive, medical, oil & gas, etc. The use of DED makes sense in specific applications where high-speed, low-resolution AM needing extensive post processing is acceptable. As a result of this, the applications for DED might be considered dull compared with the jet engines and artificial limbs that one associates with PBF machines. Often DED applications present as repairs or feature enhancements. According to one source, parts repaired with DED can actually have enhanced material properties so they are better than when first built.

DED can in fact be looked at as a way to automate the manual welding process that has been used for 100 years. DED forms a metallurgical bond like welding but with an extremely small heat-affected zone. This, SmarTech believes, is a major market opportunity for DED, because there is a huge addressable market for DED in the higher end of the welding market. The materials used for DED today are mostly just off-the-shelf welding materials, which helps lower the cost of DED materials compared to materials for other AM processes.

DED is already fairly widely used to repair military equipment. For example, the US Army Anniston depot has used DED to repair engine components for the M1 Abrams tank. This allowed the Army to repair rather than replace worn engine components saving over $5 million per year. DED has also been used extensively to repair turbine blades, satellites and other high-end equipment. Often this repair process is done by defense contractors or by companies working directly for other large industrial companies. As an aside, the connection to the defense industry is supposedly one reason that DED is not as well-known as it might be. Because it may be seen as a military process, it is not as well “advertised” as other processes.

This does not mean that every little metal shop is a prospect for selling a DED machine to. This is clearly not the case. However, for larger welding operations, buying (say) a $250,000 machine that yields better control and repeatability in manufacturing may be an attractive option. More recently, advances in multi-axis robotics and advanced CAD/CAM have allowed more complex shapes to be built onto surfaces. Feature addition can be valuable if the printed feature is expensive to produce conventionally.

Vendors Galore

The ubiquity of repair applications is good news for the future of DED and SmarTech is also impressed by the list of DED vendors: 3D Hybrid Solutions, Additec, BeAM, DM3D, DMG Mori, ELB-Schliff, Evobeam, FormAlloy, Hybrid Manufacturing Technologies, InssTek, Mazak, Norsk Titanium, Okuma, Optomec, Okuma, OR Laser, Prima Additive, Prodways, Sciaky, Trumpf, and Lincoln Electric.

This is a list which includes both major CNC firms and AM firms. In some contexts it is possible that DED is cutting into the market of PBF machine makers.

In just a few short years, 3D printing of aluminum has gone from something that was seen as a relatively challenging feat without a whole lot of commercial activity outside of a few users who had perfected some ‘black magic’ additive manufacturing (AM) expertise with the metal, to one of the fastest growing metal groups in additive manufacturing in 2018. Demand for aluminum additive solutions isn’t slowing down, and growth is likely going to continue ramping up. If you’ve been following metal AM at all over the last year, none of this probably sounds like news to you. When you take a high enough view of the industry, however, aluminum printing still looks pretty underrepresented. There are several reasons for this. If you’re just comparing shipment numbers that are based on the mass of metal powders sold (as is common in the industry), aluminum as one of the least dense metals commonly printed doesn’t show up with big shipment numbers compared to dense materials like steels or nickel superalloys. If you take the mass of the material out of the equation, SmarTech estimates that aluminum printing accounts for about 10 percent of all metal printing today. Clearly, that percentage is higher in certain industries that have adopted metal AM and lower in others.

Printed aluminum has always been in highly sought after, but it hasn’t been until the last couple of years have a wider group of users mastered the processing requirements to get stable, productive, high quality aluminum parts. Some users have been aided by the machine community who have collectively expanded their process parameter sets to include aluminum as an ‘approved’ or ‘optimized’ material for use in their systems for customers who don’t want to invest the R&D time to stabilize the process themselves.

But there’s also suddenly a lot more options for aluminum printing using powder bed fusion. Even through to today, one alloy has accounted for a huge proportion (essentially 100 percent in the recent past) of aluminum AM. Even though they still aren’t too widely used just yet, there’s now real commercial support for cast, wrought, and specialty aluminum alloys. Aluminum is special amongst other AM metals in that a high percentage of materials need specific composition tailoring just to form properly in powder bed fusion –even if they’re based on common aluminum alloys used in other manufacturing processes. This has likely helped (finally) spur more material developments in specialized aluminum alloys that have been designed specifically for additive manufacturing, like Scalmalloy and Addalloy.

It is this material expansion in a very additive-centric or specific nature that, when we extend the industry timeline out several more years, we can arrive at a conclusion –aluminum printing is key to the future of the metal powder bed fusion technology market. In an industry that will increasingly diversify in terms of metal additive process types, there will at some stage be competition for machine investment dollars amongst the expanding community of metal AM. Even though processes like metal binder jetting and directed energy deposition aren’t all that comparable from a technical standpoint, we’re already seeing some of these competitive effects as users want to explore the possibilities of new metal processes, especially those that still face some challenges with expanding their scope of use in metal powder bed fusion.

Aluminum printing is almost entirely based in powder bed fusion technology today, and with the rise in process-specific aluminum materials, is likely to become a highly defensible zone for this specific group of metal AM technologies to play in. Development of a good solution for bound metal deposition or metal binder jetting of aluminum is probably an inevitability at this point, with Stratasys, Desktop Metal, ExOne, and potentially several others already working on it to some degree. However, there has no doubt been a shift in what we’ve seen many of these bound metal companies begin their commercial operations saying (“print in more materials like aluminum!”) and what they’re actually building businesses around several years in (steels). And even if some aluminum materials become commercially viable in terms of bound metal sintered parts, aluminum powder bed fusion materials are already moving into uncharted territory with alloys based on rare-earth and transition metal alloying elements.

This leaves powder bed fusion not only as the key –and possibly sole –additive technology for aluminum printing at scale, but also as a tool which can unlock new capabilities with aluminum parts not found using traditional methods like casting or machining. Thus, powder bed fusion and aluminum may be strongly linked well into the future as a major opportunity with benefits and capabilities that no other manufacturing technology –additive or not –can match. This will certainly aid in building business cases in aerospace, and in the future possibly other industries.

Despite what headlines, technologists, and marketing executives would have you believe, the metal 3D printing “race” is a marathon, not a sprint. To continue with the metaphor, we’re probably in about mile 10 of the race today –certainly not at the beginning anymore, but also quite a long way from the end. We are now about twenty three years since the first commercial metal powder bed fusion (PBF) systems came into view. The race has gotten exciting in the last few years, with a lot of competitors now fully invested and looking for victory –or at least to be relevant twenty years from now.

With so many closely comparable suppliers of metal powder bed fusion equipment now vying for market share, this begs the question, who has what it takes to make it? Everyone in the race today is working toward similar visions of an “Industry 4.0” future that hinges on metalworking going fully digital and highly automated from end to end, from prototyping all the way up to scaled production, with varying levels of customization capabilities based on industry needs along the way.

Before we answer the question posed in the previous paragraph, we note that metal PBF isn’t the only viable metal AM process. But for now, metal PBF has major standout traits. First, PBF now has a slew of suppliers all operating with relatively similar processes who are now searching to some degree for elements to differentiate themselves from the pack; second it accounts for about 80 percent of all installed metal additive technology in the world today; and third; it has the greatest potential to be a “jack of all trades” metals manufacturing process that excels in many aspects and can fulfill the stated vision of the broader industry.

Here’s our current predictions on how the metal AM powder bed fusion race will shake out, and what elements will keep the players relevant a decade from now; as well as who might fall to the back of the pack to be eventually acquired or even become a competitive casualty. There are plenty of companies not mentioned in this piece. Also, just about every competitor has some elements we applaud and some we find troubling. Those that are mentioned below are the exceptional, while those that aren’t mentioned, couldn’t readily be identified as a long-term leader or potential die-out.

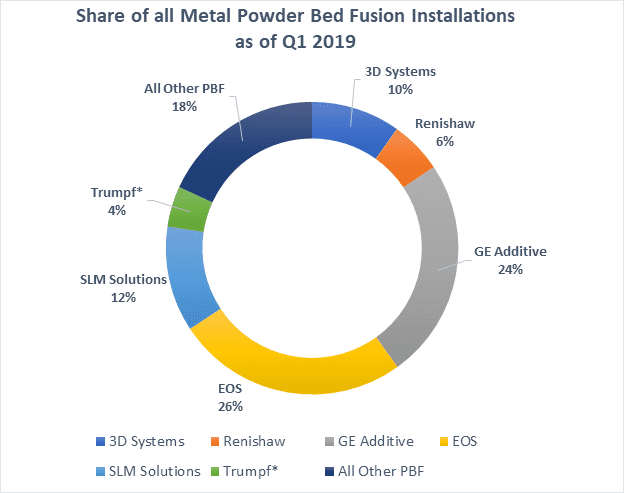

Source: SmarTech Analysis 2019 Metal Powder Bed Fusion Market Deep Dive Report

As of the end of the first quarter of 2019, EOS still controls the largest number of metal PBF machines installed worldwide, by about 400 systems compared to its next closest competitor. If there were any single factor that could aid in a company’s longevity in the space, this would probably be the most important one. Any developer of a third-party technology or solution to aid in the PBF workflow is going to make sure its solution works with EOS machines, simply because they’re the most common. That gives EOS a certain “market pull” that nobody else can claim.

However, it’s not just about the numbers. EOS has a diverse product lineup of metal machines that range from capable entry-level systems, to workhorse single-laser systems of medium and large sizes, to modular multi-laser systems that can operate in parallel architectures for continuous use and automated factory-like implementations. This in itself isn’t unique in the marketplace anymore. But when combined with the consulting prowess of Additive Minds (EOS’ customer consulting division), EOS’ technology for quality assurance and process monitoring, and its proven ability to innovate on the technology side, it establishes EOS’ prowess. EOS isn’t going anywhere for a long time.

The next big thing from EOS might be an adaptation of its Laser Pro Fusion concept, which utilizes many smaller, less expensive diode lasers, for metal PBF. Even though EOS is more specialized in one metal additive process, if any firm has the capability to totally reimagine the nature of the process and commercialize it into a manufacturing tool, it’s EOS.

GE has had its share of corporate problems in the recent past, and some in the industry have speculated that there’s no guarantee that GE’s additive division won’t be divested if GE decides to shed holdings to focus down on (what GE might consider) core businesses. However, not only is this purely speculation, it’s actually probably not at all likely to happen, because additive is increasingly at the core of GE.

Herein lies GE’s biggest market advantage –it has been the biggest user of its own technologies (and others) for a long time. In its power generation division, GE has begun to demonstrate what leveraging additive manufacturing in a major way can accomplish. GE has demonstrated this with the Additive Manufacturing Performance upgrade to its GT13E2 gas turbine announced a year ago –the production and installation of additively manufactured heat shields and turbine vanes which, through design innovation and AM, increase efficiency of an existing turbine. This is one of the best demonstrations of advanced additive innovation in the world. Now, whether or not GE Additive can sell machines and services to customers to help them achieve the same level of innovative implementation in their additive strategies is still up for debate.

But to alleviate any remaining concerns about GE Additive’s prospects, we would point to their second-to-none diversification of offering in the metal AM market. Its laser powder bed fusion segment has the broadest product portfolio in the industry, so that no opportunity within the scope of PBF is left on the table. This will be expanded even further with the commercialization of GE’s ATLAS extra-large format offering in the coming years. GE also still has a stranglehold on the electron beam powder bed fusion market, and its subsidiary Arcam’s performance in the last quarter was stellar. Add in the in-house metal powder offering, and the soon to be commercialized industrial metal binder jetting technology, and GE Additive is definitely looking to not only be around at “Mile 26” of the race. It is clearly hoping to win. And by most metrics it is well positioned to do so.

Perhaps GE’s only weakness relative to its competition is that it’s part of a mega-corporation. Although this certainly has its advantages in terms of resources and building internal expertise, smaller specialist competitors can be nimble and flexible, capturing market attention with the full weight of corporate focus on one mission.

Trumpf’s advantages in the laser PBF market are numerous, suggesting the potential to thrive over the long term in the market, but they just aren’t there yet in 2019 compared to the other companies in the “winners” category. However, when taking their entire business into consideration (of which additive is only a portion), Trumpf’s prospects look very good.

As an expert in the development and implementation of laser-based manufacturing technology, Trumpf makes and develops its own laser technology. It works in close collaboration with the most influential research institute in the metal AM market, Fraunhofer ILT (though many of its competitors do as well to varying degrees). Examples of the level of innovation in laser technology and development that can quickly be applied to AM by Trumpf and its partners at Fraunhofer include the green laser technology announced for the TruPrint 1000 system in processing copper or precious metals in 2018, or the high speed laser metal deposition process developed in conjunction with Fraunhofer and commercialized in late 2017.

In fact, a consistent customer sentiment on Trumpf’s additive technologies is that having the laser itself made by the machine manufacturer creates an excellent synergy for parameter developments, and potential replacements as optical systems wear out.

The list of elements that Trumpf lacks today compared to the powder bed industry leaders is rapidly shrinking as well. Though it has only two primary systems today which are widely supported in the market, its 5000 series system is now fully commercially available and expands Trumpf’s offerings into the realm of highly industrialized powder bed fusion with multi-laser capability. More recently Trumpf’s additive division has also begun offering powder distribution and parameter development services to its customers, as well as a connected series of ancillary handling products for powder and part management.

Compared to close competitors, Trumpf has broader company resources and manufacturing implementation experience, but remains exceptionally dedicated to industrializing metal additive manufacturing as the future of the company.

Source: SmarTech Analysis 2019 Metal Powder Bed Fusion Market Deep Dive Report

It’s no secret that SLM Solutions has been struggling during the recent period of market slowdown in metal PBF, with financial results falling, despite the fact that an excellent rebound seemed on the way after a dramatic failed GE acquisition bid in 2016. Taking into consideration the GE debacle, slumping performance, and leadership turmoil, SLM Solutions’ issues are at least in part due to consistent failures in leadership. By most accounts, SLM’s core technology is solid, and the company has a reputation for selling machines which are stable and productive.

However, poor leadership isn’t the only problem –after all plenty of companies in the 3D printing industry at large have had their share of leadership failings. The company’s product offering is comparable to much of the pack of competitors, but does not quite measure up to industry leaders, with the vast majority of its revenues coming from just two hardware products.

SLM Solutions also may be significantly lacking in close links to customers, something which all of the winners in this industry share in common. There is no significant or unified application consulting group, no marketed or known offering for machine customization for customer specific solutions, no opportunities to build customer relationships by offering parts printing as a service while customers grow to purchase machines in-house, preferring to leave it up to customers to develop solutions on their own through an open and accessible machine architecture. While this of course offers some advantages to those customers who are dedicated to doing a lot of the total process development, strategy, application business cases, themselves, this is a lot to ask of customers who ultimately want to fully utilize machines to be making parts and seeing return on their investments. To be clear, successful entities don’t have to have parts printing services, operating customer consulting groups, or a customized machines offering. But those that want to survive should probably have some business elements that link them more collaboratively to customers without requiring them to do all the heavy lifting.

But perhaps the most glaring difference between SLM Solutions and it’s three closest competitors appears to be a lack of long term technical vision for powder bed fusion technologies demonstrated by future pipeline projects. EOS was first to market with its parallelized architecture concept, with GE Additive’s Concept Laser very close behind. Today these companies have visions for extreme large format powder bed fusion based on moving exposure zones, or highly productive powder bed fusion concepts based on alternative laser types and laser control (like Laser Pro Fusion from EOS). SLM Solutions is less innovative in its vision, with its most potentially disruptive project underway being a sixteen-laser system which seems unimaginative compared to what others are developing.

Renishaw is a company that has made good strides in the last three years building up its powder bed fusion business from close to nothing into something that resembles a legitimate challenger to some of the German powerhouses, especially with its latest AM 500Q quadruple laser system.

However, out of all of the players in laser powder bed fusion who are worth mentioning today as challengers to the historical leaders, Renishaw still probably has the most limited product portfolio in the market. The company sells three standalone system configurations, all of which are roughly the same build size. Legacy Renishaw printers in its now retired AM250 platform are widely deployed in research institutes, and its AM 400 printer it now sells is clearly a slightly more robust version of that system, with design elements mainly a call-back to the standalone R&D and prototyping systems of the early 2000s, but with some modernizations in the material handling and filtration.

Meanwhile, it’s 500 platform comes in a single laser and quadruple laser configuration. It’s 500Q quad laser system appears to be quite capable, and Renishaw should be applauded for designing its own optical galvo components made via additive manufactured aluminum. The build volume of its quad laser system is the same as it’s other two systems at 250x250x350mm (well not exactly, the AM400 is 250x250x300), which is a fairly modest size for a four laser system, but this in part allows all four lasers to track the entire build chamber, and also gives it some distinction amongst other quad laser systems which tend to have larger build chambers.

As far as hardware goes, however, that’s it. More recently Renishaw has begun offering a range of ancillary supplies, as well as distribution of metal powders under what appears to be a ‘white label’ style agreement. To its credit, Renishaw does have some in-house developed process monitoring components, and also operates ‘Solution Centers’ which provide customers access to machines and experts to help develop applications and build business cases, though these are clearly not production centers in the traditional ‘parts printing services’ sense.

Overall, Renishaw looks like a company that can succeed in the industry, but it really needs to expand the scope of its AM efforts quickly if it wants to continue to gain share and remain relevant well into the future. The AM business is only a small portion of corporate Renishaw, which is also involved in the global metrology and healthcare solutions markets (among other things), so we could easily see Renishaw’s additive business unit getting spun off at some point in the future should growth become difficult in a crowded marketplace.

It almost seems inappropriate to put DMG Mori on this list because of the lack of impact this company has had in the powder bed fusion market. But because of DMG Mori’s status in traditional manufacturing, there exists potential for the company to build a significant additive business with PBF, but not any time soon. In the hybrid directed energy deposition metal additive manufacturing, DMG Mori has been quite successful and holds a very good reputation, and its overall prospects remain quite good. In fact, the company would very likely find itself on a list of ‘Winners’ for directed energy deposition additive outlooks

DMG Mori’s PBF technology was lacking in capability when the company acquired the rights to develop it further and sell systems from Realizer GmbH, and since then, some progress has been made. However, we think that there is likely little hope for DMG Mori to grow its PBF business beyond a niche offering that exists almost solely as a compliment to a broader metalworking technology portfolio that is based on laser deposition welding and machining.

In 3D printing, its common to get big news weekly. At least, that’s been the trend the past eight years (as long as I have been in this industry). Probably the biggest recent news in 3D printing was the latest funding round closed by Carbon, in which $260M was pledged by various big-name groups, bringing the company’s total fundraising since its inception to a reported $680M+.

This poses several questions which perhaps could be best summarized by a broader one –is Carbon really a startup anymore? Should it now be considered one of 3D printing’s heavyweights, alongside much larger, more historied competitors such as 3D Systems, HP, Stratasys, and the like?

Why the Money?

In order to put some context behind Carbon’s excellent fundraising performance, it’s important to understand the reasons that this business might attract big money.

As a company, Carbon has crafted a catchy, compelling brand and message all the way from its beginning. It’s very easy to see how big investors might be wowed. Carbon seems to inherently know the things to say, and what to highlight, in order to secure the dollars.

Beyond talk and branding, SmarTech believes that Carbon is sitting on something special. Carbon’s value proposition is often conveyed in a way that is meant to be cool, catchy, an in tropes that are becoming a bit tiresome in the industry (10x faster speeds!). But the reality is that Carbon’s technology platform and its business model really are setting Carbon apart from the rest of the industry.

In particular, we think that investors aren’t getting a full picture of Carbon if they don’t understand the role that Digital Light Synthesis (Carbon’s slickly named printing process) might play in the broader world of polymeric 3D printing, and even broader plastics manufacturing.

Such “high speed” or “layerless” photopolymerization technologies are perhaps the most interesting thing to happen to plastic 3D printing since, well, the invention of the traditional photopolymerization printing technologies, which were the first true 3D printing technologies.

Carbon isn’t the only firm to offer this type of technology for a 3D printing platform – at some level, 3D Systems and EnvisionTEC also offer a similar process being leveraged in different ways and with relatively minor mechanical differences. Newcomers like Nexa3D and Origin also have relatively similar printing capabilities but aren’t as far along in establishing a serious 3D printing business as the other firms mentioned above.

At their core, these processes utilize a projector and some form of curing inhibitor mechanics to eliminate the layer-by-layer printing dynamic. What sets Carbon apart today, however, is its control of the printing mechanics combined with a mastery of the chemistry required to create optimized printing materials for big-time applications.

Layerless photopolymerization does appear to be positioned to be potentially competitive with injection molding to a serious degree, especially if it is supported by material development, competent software to manage the complexities of a digital production process, and sufficient customer support. Through this lens, Carbon is probably the most advanced of its peers, but it still has some ways to go.

So, it makes sense for investors to put money into this technology. There are a huge number of players in plastic 3D printing attempt to advance the technology into the territory of injection molding, but Carbon is one of the furthest ahead in terms of taking business from molding technologies.

Carbon: A 3D Printing Heavyweight?

Carbon isn’t yet a 3D printing heavyweight, and this should not come as a shock to anyone, especially its investors:

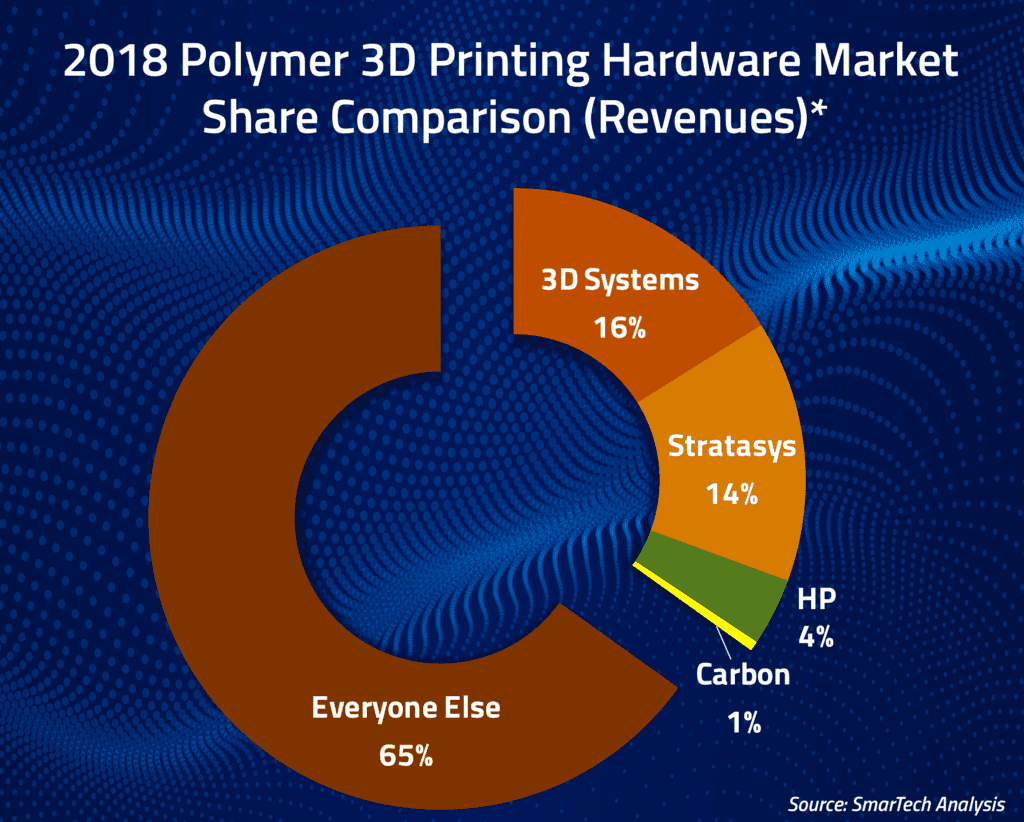

Compared to 3D Systems, Carbon doesn’t have near the product portfolio (to say nothing of its global network of resellers and parts printing service partners), or the expertise in high impact markets like healthcare. However, here I would champion Carbon’s abilities in the consumer goods market, an area in which it has leapfrogged much of its competition. In 2018 3D Systems held a 16% share of the market.

Compared to HP, which is closer to Carbon in terms of breadth of technology portfolio, it goes without saying that Carbon doesn’t have the global manufacturing resources or sales channels of a $50 billion company. Little to compare there. However, Carbon’s recently raised funds are expected to go largely towards an international expansion. HP is pushing its technology into familiar markets for powder based plastic printing, while Carbon is mainly charting new territory for photopolymer-based printing (if you exclude the more recently launched dental business). In 2018 HP owned 4% of the market.

There aren’t many good comparisons between Carbon and Stratasys. Carbon appears to be growing very rapidly after reporting significant increases in printer utilization metrics from its customers over the last year and has told SmarTech to be adding new dental lab customers almost weekly. Stratasys hasn’t been profitable in nearly six years, has been searching for a CEO for over a year, its revenues have been stagnant for four years, and six years ago probably made one of the most grossly over-valued acquisitions in recent tech industry. Still, the company owned a 14% share of the market.

Comparing the company’s revenues in its targeted segment vs the major players shows Carbon to be a very minor player. In 2018 it garnered .6% of a $1.744 billion (USD) market. However, roughly 2/3 of the market exists outside of 3D Systems, Stratasys and HP and each company has their own vulnerabilities.

Heavyweight or not, Carbon has successfully convinced investors that it compares favorably to the AM industry giants in various ways, at least sufficiently for those investors to open wide their checkbooks.

What sectors are showing best opportunities this next year in metal AM?

Demand for metal AM is in a bit of an unsteady period while the global economy and the AM market shake out a bit over the next several quarters. What needs to be understood is that for the longest time, there’s only really been one widely commercially accepted metal additive process (metal powder bed fusion and its variants), and everything beyond that was niche with appeal only to very specific use cases and customers. Now, there three viable technical segments of the market, and this has got companies looking at things differently, which at some level is changing the demand pattern for the industry.

It’s still acceptable to say that metal powder bed fusion is the driving force of the industry today in 2019, so with that in mind, the biggest opportunities are still going to mostly be influenced by this technology group. Aerospace and healthcare are the big traditional areas here. We’re hearing mixed results for the demand pipelines for these technologies in the near term, with some companies reporting their pipelines are either looking more positive than a quarter or two ago, or are at all-time highs, while others are indicating that their pipelines are a bit weaker this year compared to the same time last year. I think the conclusion we can draw from this is that the competitive structure of the industry in powder bed fusion is starting to come into play a bit more and that demand hasn’t increased at the same rate that the number of suppliers with well-positioned technologies has –yet.

If the pipelines are a bit up-and-down, that probably means that the traditional adopters are still a little hesitant on where to go next with additive and how quickly. I would still say aerospace and healthcare will be big market drivers in 2019, but I expect that there may be a bit of a focal shift to oil and gas and industrial components than in the past to supplement sales. While the landscape of oil and gas isn’t exactly bright right now companies are at least now able to see the benefits of metal additive which should drive demand in this sector.

Industrial components, equipment, and products are a broad area and as the awareness and mastery of metal additive technologies filtered down through institutions and corporate R&D labs we’ll start to see more demand from general industry. I don’t think that 2019 will necessarily be the year that the auto industry really takes off for metal additive because of the more challenging market situation in that industry right now, and the still relative immaturity of new metal binder jetting systems which hold the best long term promise for big integration into auto manufacturing.

What headwinds do AM suppliers need to address?

AM suppliers need to start looking at the big picture. I think most companies over the last decade have accepted that their specific metal additive process isn’t the solution for everything. But, what needs to happen now is taking that realization and acceptance to another level, and understanding that metal additive technologies are maturing to a stage where, when taken in aggregate across all the process types that are gaining real steam, metal additive could play perhaps a much bigger role than they might have realized before if customers begin applying each process style where it fits best.

Bound metal deposition solutions from the likes of Markforged and Desktop Metal are making great strides in cost effective prototyping and speeding time to market, all in a package that is fairly accessible.

Metal binder jetting is trending towards being highly productive and scalable for applications that have huge volumes, slightly lower mechanical requirements, and parts made from steels.

Directed energy is continuing to redefine how companies can keep products and systems fielded for longer by being utilized for repair and part augmentation.

And finally, as mastery of metal powder bed fusion continues to increase in the user community, it’s becoming a great candidate for producing low to medium volumes of robust, complex, next generation parts and systems of parts for everything from production to aftermarket and spares especially in high performance materials.

We strongly believe that there is going to be a role for each of these processes to play and customers are going to better understand that. When you piece all the roles together, it’s a huge potential impact. Suppliers should be looking into capitalizing on that big vision and having a tailored solution set for the whole manufacturing chain, not just trying to sell one process to all areas.

Which companies do you see as leading, which ones are lagging?

MarkForged and Desktop Metal seem to be flourishing because they’ve brought viable products to market that are bringing some accessibility to metal AM. They have helped unlock new customer segments who may have found powder bed fusion technology out of reach or not a good fit for their needs/working environment.

GE Additive has only just begun to tap the potential of their group but longer term they are taking a very good approach. Part of that success is related to their decades long experience as a user of their core technologies, and part of it should come from the strategy of building a multi-solution technology portfolio. In the next one to two years they’ll be strong in laser powder bed fusion, electron beam powder bed fusion, and metal binder jetting (if not more solutions).

Companies like EOS who are specialists in one process are going to have to keep pushing the boundaries if they want to survive long term, and here I would say that EOS specifically is at least moving in the right direction. They have an impeccable history of technical innovation and their latest works in Laser Pro Fusion (using many diode lasers) demonstrates that.

Companies that are lagging are those which aren’t positioning themselves for a future where different metal additive processes are going to have clearly understood value propositions within a broader scope of AM implementation. For example, a year ago most in the industry didn’t see much inter-tech competition between bound metal processes and powder bed fusion because of the very different part properties, materials, and economic considerations for each. However, if you are a company that has historically had success selling powder bed fusion equipment for prototyping applications, your value proposition is now significantly impacted because there are now other inexpensive and accessible bound metal deposition technologies. Said technologies can capitalize on unmet demand for cost effective prototyping in metals that powder bed fusion technology was seemed as overpriced.

When will a fully integrated solution set be a requirement for any company serious about being a player in metal AM?

Not this year, and not next year, but by 2021 there’s going to be a lot more options and acceptance of metal binder jetting for production and directed energy deposition for repair of high value parts in a serial fashion. Maybe suppliers aren’t too worried about other technologies and processes infringing on their territory, but the opportunity cost of missing out on the new growth these will be a huge mistake. This also goes for having solutions that aren’t focusing only on the ‘factory of the future’ where the potential users are going to have to commit to tens of millions in investment in these factories just to get to a point where the technology is cost effective. What I like most about the compact industrial printer segment being led by bound metal deposition is that it’s opening metal AM to more users –these users are undoubtedly going to want to scale up their use once they’ve had a little time to gain some process expertise and experiment with implementation. They’re going to want to scale up not just in terms of volumes, but to solutions that provide different benefits that span the spectrum of manufacturing innovation that AM can provide.

How does AM play into considerations for potential looming economic downturns? How do vendors message this?

From a historical perspective, we’ve seen how economic downturn can hit the AM industry. 2009 is generally accepted as the only year in the last decade that the industry actually declined. Optimistically, however, there was a pretty quick recovery over the next three years which I think speaks to the real value of the technology. Also, I think we’re in a very different point of the industry today than we were then, when things were still almost entirely driven by rapid prototyping and research. The more global manufacturing companies embrace Industry 4.0 innovation strategies –of which additive manufacturing are at the core –the more insulated AM becomes from economic turmoil, because even as overall manufacturing activity might shrink, additive programs will continue to increase. We see this today in the energy and oil and gas industries which have been challenged for a couple of years, but by all accounts, additive programs remain growing in these areas.

More importantly though, is for companies to understand that the benefits of implementing AM can help them weather economic uncertainty as well. The ability to introduce flexibility into a supply chain can make companies more nimble and able to redirect resources more effectively.

A great example of AM’s ability to withstand economic turmoil long term is what GE power has done with some of its gas turbines. Using additive, they are now offering ‘upgrade packages’ to existing customers that integrate some newly designed components made via additive manufacturing which increase performance and longevity of the system. This is a perfectly sellable solution during economic downturn because customers using these turbines will get greater efficiency and reduce their costs. The role that additive plays in this scenario is that it provides a performance enhancement to the system that isn’t achievable with traditional manufacturing, and it also is positioned as an upgrade to existing equipment so AM can be flexibly applied as the production process as upgrades are ordered.

In SmarTech Analysis’ new report, “The Market for Lasers in the Additive Manufacturing Sector: 2019-2028” we analyze how multilaser machines are having a positive impact throughout the AM supply chain from laser manufacturers, who get to sell more lasers as the result of multilaser machines, to the 3D printer suppliers themselves. From the end-user perspective,…..

Over the past quarter, SmarTech has been releasing a series of insightful data-backed market insight briefs on various sectors of the metal additive manufacturing market, focusing on specific types of metals which are driving (or expected to drive) metal AM over the next decade. The release of these shorter, material-specific briefs will culminate in the…..

Metal additive manufacturing continues to be one of the most influential next-generation technologies. While metal 3D printing is a hot topic in the industry, most of the focus has been on large-scale production and throughput rather than accessibility. For those new to metal 3D printing, entering into additive versus subtractive manufacturing can be a daunting…..

Footwear 3D printing is set to grow into a 6.3 billion overall revenue opportunity over the next 10 years (according to the latest report from SmarTech Analysis). If this consumer product segment will deliver what many are now quite convinced it will, most of the credit will likely go to five major footwear AM companies…..