The global manufacturing market seems to be in a state of flux, throwing the metal additive sector into a totally new realm of existence. The last significant global manufacturing downturn in 2009 came largely before metal additive technologies had established itself. In 2009, AM metal implants were only just beginning to see their earliest patients and metal AM in aerospace was still entirely in the R&D lab. While it would be premature to declare anything definitive about metal AM, we believe it’s time to view metal additive technologies, and their near-term futures, from the standpoint of both actual and attainable applications from which to base growth projections and investment decisions in what is a tightening manufacturing scenario.

SmarTech maintains that additive technologies will play a key role in creating more agility and responsiveness in global metal manufacturing activity to allow better weathering of global economic speed bumps. However, the advantages aren’t truly universally applicable to all given the relatively high barrier to entry that remains, the lower overall state of commercial readiness of emerging high-potential technologies, and the resulting lack of vision and understanding on how to apply each mainstay technology effectively to create more nimble, cost effective metal component supply chains and eliminate costs.

Of the three primary families of metal additive technologies, powder bed fusion variants remain the most widely utilized and industrialized systems with varying degrees of ‘factory readiness’ depending on the provider. Directed energy deposition systems have played a niche role for many years and continue to subtly infiltrate manufacturing deployments by integrating with CNC technology for hybrid use cases. Finally, bound metal printing variants, which consist of both binder jetting and deposition based systems, both share a common metallurgical principle of final-stage sintering and are still perhaps just coming onto the horizon of metal additive manufacturing (but with much potential).

Manufacturing downturns are inevitable. Whether next year or years from now, metal additive technologies have a unique opportunity to present a value proposition to the manufacturing community as tools to help weather these recurring challenges. SmarTech Analysis has just produced the first ever unified global analysis on metal additive manufacturing parts & applications. Using the perspective of production volumes of metal parts produced additively by functional application, we can demonstrate what is likely to become the potential future of each of the primary metal additive technologies, as well as emphasize their potential value as solutions for leaner manufacturing.

Despite what headlines, technologists, and marketing executives would have you believe, the metal 3D printing “race” is a marathon, not a sprint. To continue with the metaphor, we’re probably in about mile 10 of the race today –certainly not at the beginning anymore, but also quite a long way from the end. We are now about twenty three years since the first commercial metal powder bed fusion (PBF) systems came into view. The race has gotten exciting in the last few years, with a lot of competitors now fully invested and looking for victory –or at least to be relevant twenty years from now.

With so many closely comparable suppliers of metal powder bed fusion equipment now vying for market share, this begs the question, who has what it takes to make it? Everyone in the race today is working toward similar visions of an “Industry 4.0” future that hinges on metalworking going fully digital and highly automated from end to end, from prototyping all the way up to scaled production, with varying levels of customization capabilities based on industry needs along the way.

Before we answer the question posed in the previous paragraph, we note that metal PBF isn’t the only viable metal AM process. But for now, metal PBF has major standout traits. First, PBF now has a slew of suppliers all operating with relatively similar processes who are now searching to some degree for elements to differentiate themselves from the pack; second it accounts for about 80 percent of all installed metal additive technology in the world today; and third; it has the greatest potential to be a “jack of all trades” metals manufacturing process that excels in many aspects and can fulfill the stated vision of the broader industry.

Here’s our current predictions on how the metal AM powder bed fusion race will shake out, and what elements will keep the players relevant a decade from now; as well as who might fall to the back of the pack to be eventually acquired or even become a competitive casualty. There are plenty of companies not mentioned in this piece. Also, just about every competitor has some elements we applaud and some we find troubling. Those that are mentioned below are the exceptional, while those that aren’t mentioned, couldn’t readily be identified as a long-term leader or potential die-out.

Source: SmarTech Analysis 2019 Metal Powder Bed Fusion Market Deep Dive Report

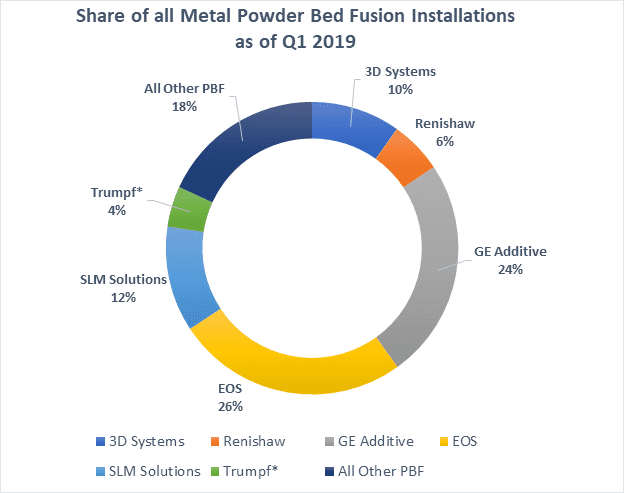

As of the end of the first quarter of 2019, EOS still controls the largest number of metal PBF machines installed worldwide, by about 400 systems compared to its next closest competitor. If there were any single factor that could aid in a company’s longevity in the space, this would probably be the most important one. Any developer of a third-party technology or solution to aid in the PBF workflow is going to make sure its solution works with EOS machines, simply because they’re the most common. That gives EOS a certain “market pull” that nobody else can claim.

However, it’s not just about the numbers. EOS has a diverse product lineup of metal machines that range from capable entry-level systems, to workhorse single-laser systems of medium and large sizes, to modular multi-laser systems that can operate in parallel architectures for continuous use and automated factory-like implementations. This in itself isn’t unique in the marketplace anymore. But when combined with the consulting prowess of Additive Minds (EOS’ customer consulting division), EOS’ technology for quality assurance and process monitoring, and its proven ability to innovate on the technology side, it establishes EOS’ prowess. EOS isn’t going anywhere for a long time.

The next big thing from EOS might be an adaptation of its Laser Pro Fusion concept, which utilizes many smaller, less expensive diode lasers, for metal PBF. Even though EOS is more specialized in one metal additive process, if any firm has the capability to totally reimagine the nature of the process and commercialize it into a manufacturing tool, it’s EOS.

GE has had its share of corporate problems in the recent past, and some in the industry have speculated that there’s no guarantee that GE’s additive division won’t be divested if GE decides to shed holdings to focus down on (what GE might consider) core businesses. However, not only is this purely speculation, it’s actually probably not at all likely to happen, because additive is increasingly at the core of GE.

Herein lies GE’s biggest market advantage –it has been the biggest user of its own technologies (and others) for a long time. In its power generation division, GE has begun to demonstrate what leveraging additive manufacturing in a major way can accomplish. GE has demonstrated this with the Additive Manufacturing Performance upgrade to its GT13E2 gas turbine announced a year ago –the production and installation of additively manufactured heat shields and turbine vanes which, through design innovation and AM, increase efficiency of an existing turbine. This is one of the best demonstrations of advanced additive innovation in the world. Now, whether or not GE Additive can sell machines and services to customers to help them achieve the same level of innovative implementation in their additive strategies is still up for debate.

But to alleviate any remaining concerns about GE Additive’s prospects, we would point to their second-to-none diversification of offering in the metal AM market. Its laser powder bed fusion segment has the broadest product portfolio in the industry, so that no opportunity within the scope of PBF is left on the table. This will be expanded even further with the commercialization of GE’s ATLAS extra-large format offering in the coming years. GE also still has a stranglehold on the electron beam powder bed fusion market, and its subsidiary Arcam’s performance in the last quarter was stellar. Add in the in-house metal powder offering, and the soon to be commercialized industrial metal binder jetting technology, and GE Additive is definitely looking to not only be around at “Mile 26” of the race. It is clearly hoping to win. And by most metrics it is well positioned to do so.

Perhaps GE’s only weakness relative to its competition is that it’s part of a mega-corporation. Although this certainly has its advantages in terms of resources and building internal expertise, smaller specialist competitors can be nimble and flexible, capturing market attention with the full weight of corporate focus on one mission.

Trumpf’s advantages in the laser PBF market are numerous, suggesting the potential to thrive over the long term in the market, but they just aren’t there yet in 2019 compared to the other companies in the “winners” category. However, when taking their entire business into consideration (of which additive is only a portion), Trumpf’s prospects look very good.

As an expert in the development and implementation of laser-based manufacturing technology, Trumpf makes and develops its own laser technology. It works in close collaboration with the most influential research institute in the metal AM market, Fraunhofer ILT (though many of its competitors do as well to varying degrees). Examples of the level of innovation in laser technology and development that can quickly be applied to AM by Trumpf and its partners at Fraunhofer include the green laser technology announced for the TruPrint 1000 system in processing copper or precious metals in 2018, or the high speed laser metal deposition process developed in conjunction with Fraunhofer and commercialized in late 2017.

In fact, a consistent customer sentiment on Trumpf’s additive technologies is that having the laser itself made by the machine manufacturer creates an excellent synergy for parameter developments, and potential replacements as optical systems wear out.

The list of elements that Trumpf lacks today compared to the powder bed industry leaders is rapidly shrinking as well. Though it has only two primary systems today which are widely supported in the market, its 5000 series system is now fully commercially available and expands Trumpf’s offerings into the realm of highly industrialized powder bed fusion with multi-laser capability. More recently Trumpf’s additive division has also begun offering powder distribution and parameter development services to its customers, as well as a connected series of ancillary handling products for powder and part management.

Compared to close competitors, Trumpf has broader company resources and manufacturing implementation experience, but remains exceptionally dedicated to industrializing metal additive manufacturing as the future of the company.

Source: SmarTech Analysis 2019 Metal Powder Bed Fusion Market Deep Dive Report

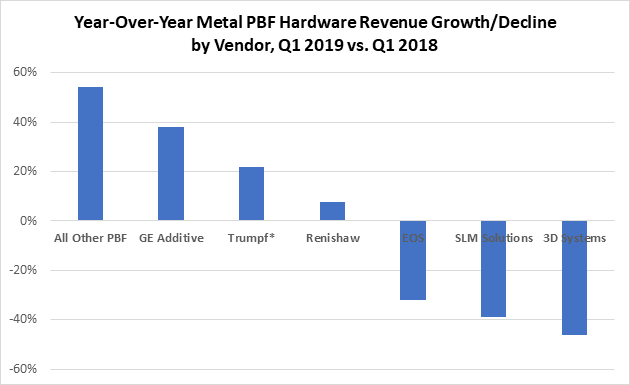

It’s no secret that SLM Solutions has been struggling during the recent period of market slowdown in metal PBF, with financial results falling, despite the fact that an excellent rebound seemed on the way after a dramatic failed GE acquisition bid in 2016. Taking into consideration the GE debacle, slumping performance, and leadership turmoil, SLM Solutions’ issues are at least in part due to consistent failures in leadership. By most accounts, SLM’s core technology is solid, and the company has a reputation for selling machines which are stable and productive.

However, poor leadership isn’t the only problem –after all plenty of companies in the 3D printing industry at large have had their share of leadership failings. The company’s product offering is comparable to much of the pack of competitors, but does not quite measure up to industry leaders, with the vast majority of its revenues coming from just two hardware products.

SLM Solutions also may be significantly lacking in close links to customers, something which all of the winners in this industry share in common. There is no significant or unified application consulting group, no marketed or known offering for machine customization for customer specific solutions, no opportunities to build customer relationships by offering parts printing as a service while customers grow to purchase machines in-house, preferring to leave it up to customers to develop solutions on their own through an open and accessible machine architecture. While this of course offers some advantages to those customers who are dedicated to doing a lot of the total process development, strategy, application business cases, themselves, this is a lot to ask of customers who ultimately want to fully utilize machines to be making parts and seeing return on their investments. To be clear, successful entities don’t have to have parts printing services, operating customer consulting groups, or a customized machines offering. But those that want to survive should probably have some business elements that link them more collaboratively to customers without requiring them to do all the heavy lifting.

But perhaps the most glaring difference between SLM Solutions and it’s three closest competitors appears to be a lack of long term technical vision for powder bed fusion technologies demonstrated by future pipeline projects. EOS was first to market with its parallelized architecture concept, with GE Additive’s Concept Laser very close behind. Today these companies have visions for extreme large format powder bed fusion based on moving exposure zones, or highly productive powder bed fusion concepts based on alternative laser types and laser control (like Laser Pro Fusion from EOS). SLM Solutions is less innovative in its vision, with its most potentially disruptive project underway being a sixteen-laser system which seems unimaginative compared to what others are developing.

Renishaw is a company that has made good strides in the last three years building up its powder bed fusion business from close to nothing into something that resembles a legitimate challenger to some of the German powerhouses, especially with its latest AM 500Q quadruple laser system.

However, out of all of the players in laser powder bed fusion who are worth mentioning today as challengers to the historical leaders, Renishaw still probably has the most limited product portfolio in the market. The company sells three standalone system configurations, all of which are roughly the same build size. Legacy Renishaw printers in its now retired AM250 platform are widely deployed in research institutes, and its AM 400 printer it now sells is clearly a slightly more robust version of that system, with design elements mainly a call-back to the standalone R&D and prototyping systems of the early 2000s, but with some modernizations in the material handling and filtration.

Meanwhile, it’s 500 platform comes in a single laser and quadruple laser configuration. It’s 500Q quad laser system appears to be quite capable, and Renishaw should be applauded for designing its own optical galvo components made via additive manufactured aluminum. The build volume of its quad laser system is the same as it’s other two systems at 250x250x350mm (well not exactly, the AM400 is 250x250x300), which is a fairly modest size for a four laser system, but this in part allows all four lasers to track the entire build chamber, and also gives it some distinction amongst other quad laser systems which tend to have larger build chambers.

As far as hardware goes, however, that’s it. More recently Renishaw has begun offering a range of ancillary supplies, as well as distribution of metal powders under what appears to be a ‘white label’ style agreement. To its credit, Renishaw does have some in-house developed process monitoring components, and also operates ‘Solution Centers’ which provide customers access to machines and experts to help develop applications and build business cases, though these are clearly not production centers in the traditional ‘parts printing services’ sense.

Overall, Renishaw looks like a company that can succeed in the industry, but it really needs to expand the scope of its AM efforts quickly if it wants to continue to gain share and remain relevant well into the future. The AM business is only a small portion of corporate Renishaw, which is also involved in the global metrology and healthcare solutions markets (among other things), so we could easily see Renishaw’s additive business unit getting spun off at some point in the future should growth become difficult in a crowded marketplace.

It almost seems inappropriate to put DMG Mori on this list because of the lack of impact this company has had in the powder bed fusion market. But because of DMG Mori’s status in traditional manufacturing, there exists potential for the company to build a significant additive business with PBF, but not any time soon. In the hybrid directed energy deposition metal additive manufacturing, DMG Mori has been quite successful and holds a very good reputation, and its overall prospects remain quite good. In fact, the company would very likely find itself on a list of ‘Winners’ for directed energy deposition additive outlooks

DMG Mori’s PBF technology was lacking in capability when the company acquired the rights to develop it further and sell systems from Realizer GmbH, and since then, some progress has been made. However, we think that there is likely little hope for DMG Mori to grow its PBF business beyond a niche offering that exists almost solely as a compliment to a broader metalworking technology portfolio that is based on laser deposition welding and machining.

At Xerox’s recent Investor Day 2019, a company that has been indirectly involved in the 3D printing industry for many years, announced its acquisition of metal additive manufacturing systems company Vader Systems and the company’s plans to develop a direct role in the market for 3D printing technologies.

Is Xerox entering 3D printing in this way, at this time, like a big fish leaping into a small, yet crowded pond? In the last two years, there are quite a few big fish which have jumped into the proverbial 3D printing ‘pond,’ and while said pond keeps getting bigger, it’s certainly becoming more and more crowded.

Statements from Xerox regarding their plans for 3D printing are very reminiscent of other major companies which have done the same in recent years, with the most direct comparison likely to be HP.

Will Xerox shake up the 3D printing market?

The company’s biggest and most direct influence for now appears will occur via its acquisition of Vader Systems. Vader, in SmarTech’s opinion, is an “aging startup” and a developer of what is claimed to be an innovative metal additive manufacturing technology based at some level on inkjet technology. While Xerox has also made some claims on its intent to bring solutions into the polymer 3D printing market including materials, printing systems, and software, we do not have concrete details as of now so we will focus on Vader and metal additive manufacturing.

What impact might Xerox have on metal AM?

From a technical perspective, Xerox’s acquisition makes some sense. The company has a longstanding history in inkjet technology, and has been a long time supplier of various elements of this technology to other 3D printer manufacturers who use it in their own printers. Vader’s technology is based on some of the same tenants of inkjet printing, with the inherent (theoretical) scalability that comes with it. With that in mind, a lot of my thoughts on how to answer the question of “will Xerox shake up the metal additive manufacturing market” end up circling back to “what are the reasonable expectations for inkjet-oriented technologies to compete against fusion or extrusion based technologies?”

There’s no easy way to answer or opine on that in a blog post, but for now, I’ve made a few observations and formed some opinions that have started to shape my thoughts on Xerox’s potential impact (keeping in mind that more concrete details are still to come).

First, the primary statements regarding Xerox’s own motives for the Vader acquisition (and apparently it’s overall upcoming 3D printing activities that will be revealed in more detail), are based on the perception that, “manufacturing customers want to use 3D printing, but the current offerings only serve the prototyping market well, not broad manufacturing.”

I consider this a very risky statement to put forth as the bases for a large investment and business strategy as this this perception is becoming rapidly outdated. I would argue that manufacturing customers are using current 3D printing technologies and they want to use them more as they are able to overcome production challenges. Suppliers and customers are increasingly messaging parts production in their AM efforts.

Xerox is also staking its position in metal AM on a technology that is decidedly not impacting the broader AM market as of yet. While there is an argument to be made for going with an outsider whose technology matches up closely with your own expertise, at this time I believe that the manufacturing community at large is ready to buy into a specific metal AM manufacturing process and work at fine tuning their processes and technologies to advance. To this end, technologies like powder bed fusion, and metal binder jetting have exponentially greater support in terms of end-to-end solutions.

There also comes a point where switching and experimenting with other metal AM methods provides diminishing returns for manufacturing customers. Xerox will have to sell the most influential users of metal AM today on a new process and at a time when we’re seeing such strong momentum behind some of the existing and more widely adopted methods.

While for now I retain a healthy amount of skepticism about Xerox’ potential success in metal additive manufacturing. I look forward to learning more about the specific solutions Xerox will bring in 2019 and beyond.

By Scott Dunham – Vice President, SmarTech Publishing

Since partnering with shipbuilding company Fincantieri last month, Australian metal AM company Titomic has signed a Material Science Testing (MST) agreement with Fincantieri Australia. The agreement is the first step in evaluating Titomic’s Kinetic Fusion technology’s viability for Fincantieri’s manufacturing processes.

As part of the new agreement, Titomic will conduct various tests on a Fincantieri specified alloy (following ASTM International Standards) using its AM process to achieve desired mechanical and chemical properties. The tests will include hardness, strength, porosity and chemistry analysis tests. The goal of these tests will be to offer insight into the material properties, performance and costs of Titomic’s additive manufacturing process.

“We are pleased to kick off this first project with Fincantieri as part of our MoU,” said Jeff Lang, CTO of Titomic. “We will be producing test samples at our new state of the art facility in Melbourne in order to conduct the stringent tests required. This is the first step towards manufacturing large marine parts on our metal 3D printers of limitless scale.”

As part of the companies’ agreement, Titomic’s technology and operational team recently made a trip to the Riva Trigoso Shipyard in Italy to learn how Fincantieri’s mechanical ship components are designers, developed and produced. Eventually, the aim is to transfer Fincantieri’s marine technology to Australia.

“Titomic’s technology combined with Fincantieri’s technology transfer program to Australia creates the potential to return Australia’s capability in mechanical componentry,” said Sean Costello, Director at Fincantieri Australia. “Our aim is to return high-value jobs to Australia, reduce costs and become sovereign as a shipbuilding nation.”

May 14: Titomic signs MoU with Fincantieri

In a world first for AM adoption by the Marine sector, Titomic signed a MoU to work with Fincantieri to evaluate the potential for the Company’s additive manufacturing process, Titomic Kinetic Fusion, to be used in Fincantieri’s manufacturing activities. Effective immediately and with a 12 months duration, Titomic’s signing with Fincantieri explores the Company’s proprietary processes to complement and improve existing manufacturing process and is the start of a synergistic partnership.

“This agreement with Fincantieri marks a significant milestone for future shipbuilding and industrial scale additive manufacturing,” said Jeff Lang, CEO and CTO of Titomic. “Titomic’s signing with Fincantieri to evaluate our Titomic Kinetic Fusion process will not only add value to existing manufacturing and repair activities, it will lead to the creation of next generation high tech vessels.”

With 20 shipyards across four continents, Fincantieri S.p.A is one of the world’s largest shipbuilding groups and number one by diversification and innovation. It is the leader in cruise ship design and construction, and a reference player in all high-tech shipbuilding industry sectors – from naval to offshore vessels, from high-complexity special vessels and ferries – to mega-yachts, ship repairs and conversions, systems and equipment production, and after-sales services.

Fincantieri also carries out maintenance and refurbishment of cruise ships – a major and growing international industry. The company is also one of the shortlisted bidders for The Future Frigates SEA 5000 program. Titomic was awarded Best Maritime Innovation award at Pacific 2017 International Maritime Exposition. This MoU affirms Titomic’s entrance into the shipbuilding and offshore industries. The initial R&D phase will take place at Titomic’s Melbourne facility.

Dario Deste, Chairman of Fincantieri Australia also commented on the deal: “We are pleased to partner with Titomic, an innovative advanced manufacturing company, to pursue new technological development, continuous improvement and value creation for all our stakeholders. The significance of this partnership examines how we can introduce new manufacturing technologies to make Australia sovereign in advanced naval technology and improve our solutions on the world-wide market.”

Since partnering with shipbuilding company Fincantieri last month, Australian metal AM company Titomic has signed a Material Science Testing (MST) agreement with Fincantieri Australia. The agreement is the first step in evaluating Titomic’s Kinetic Fusion technology’s viability for Fincantieri’s manufacturing processes. As part of the new agreement, Titomic will conduct various tests on a Fincantieri…..

Digital Metal’s unique high-precision metal binder-jetting technology continues to raise great interest in the AM field. The UK’s renowned center for innovative technology, the National Centre for Additive Manufacturing (NCAM), has just decided to add a Digital Metal printer to their already extensive range of advanced manufacturing equipment. The NCAM is part of the Manufacturing …

Sciaky, Inc., a subsidiary of Phillips Service Industries, Inc. (PSI) and leading provider of metal additive manufacturing (AM) solutions, have entered a strategic partnership with Concurrent Technologies Corporation (CTC) to support a growing demand for high quality, large-scale additively manufactured metal parts. CTC will offer Sciaky’s industry-leading Electron Beam Additive Manufacturing (EBAM) metal 3D printing technology to its diverse range of …